Falko Ueckerdt

Falko UeckerdtTechno-economic assessment (TEA): simple calculations, deep insight

Techno-economic assessment (TEA) is a widely used—and comparatively straightforward—method for comparing the costs of providing an energy or material service across alternative technologies, processes, locations, or supply chains.

In our work, we use TEA not only for direct cost comparisons, but also as a tool to uncover deeper, system-level insights. The two examples below illustrate what we mean.

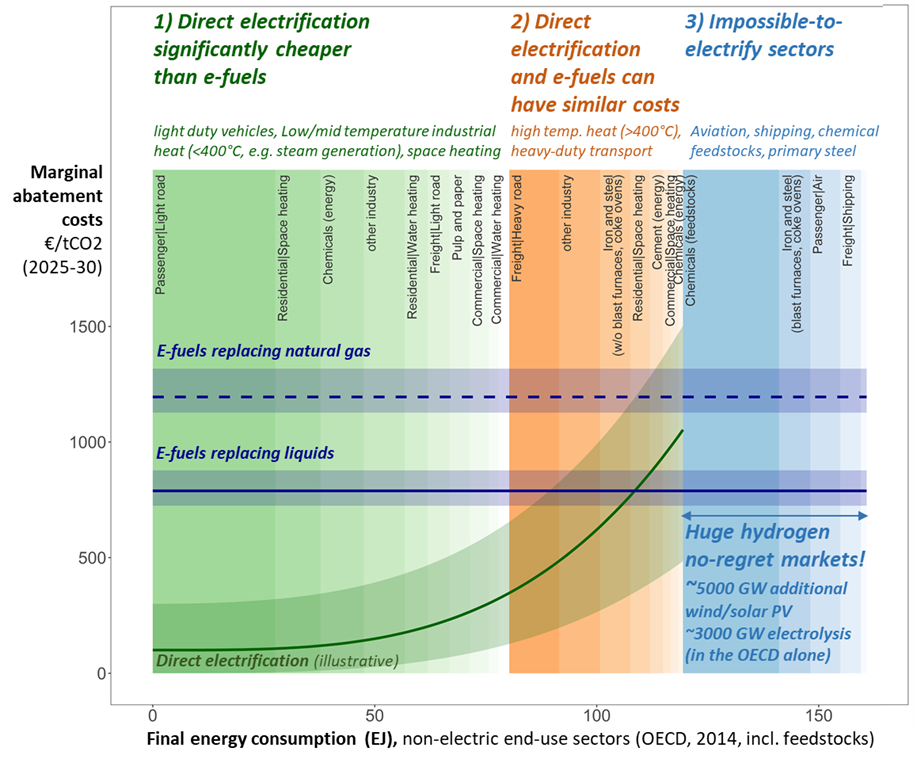

Example 1: Overlapping MACCs reveal where e-fuels make sense—and where they don’t

Marginal abatement cost curves (MACCs) are an established concept. In our Nature Climate Change paper on e-fuels, we advanced this approach by overlapping multiple MACCs across different mitigation options. Comparing MACCs for direct electrification and e-fuels across sectors helps identify where e-fuels are cost-competitive and where they are not. We refer to this as a “merit order of e-fuel applications.”

Publication: Ueckerdt et al. (2021) Potential and risks of hydrogen-based e-fuels in climate change mitigation. Nature Climate Change. https://www.nature.com/articles/s41558-021-01032-7

- Applications where direct electrification is clearly cheaper (green area)

Direct electrification is substantially less costly—for example, battery-electric mobility for cars and light-duty vehicles can reach cost levels comparable to fossil mobility (petrol and diesel). In these applications, e-fuels are unlikely to become competitive. - Applications where electrification may be complemented by hydrogen—and niche e-fuels (orange area)

In some cases, direct electrification could be supplemented by hydrogen and, potentially, e-fuels in niche roles, such as long-haul heavy-duty trucking and selected very high-temperature industrial processes. - Large “no-regret” markets where electrification faces hard limits (blue area)

In sectors where direct electrification is constrained—most notably aviation, shipping, and chemical feedstocks for basic chemicals—e-fuels can play a major role.

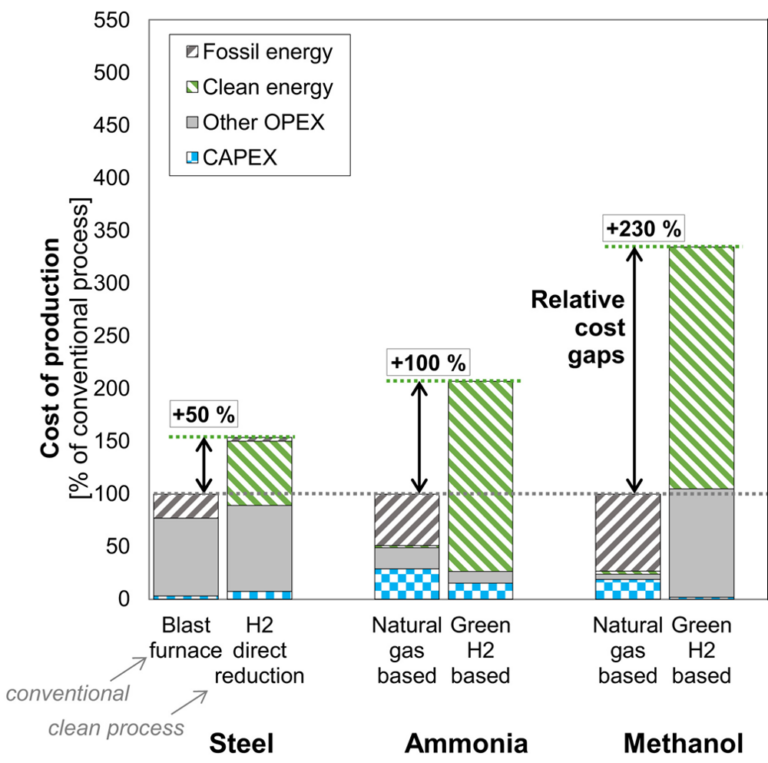

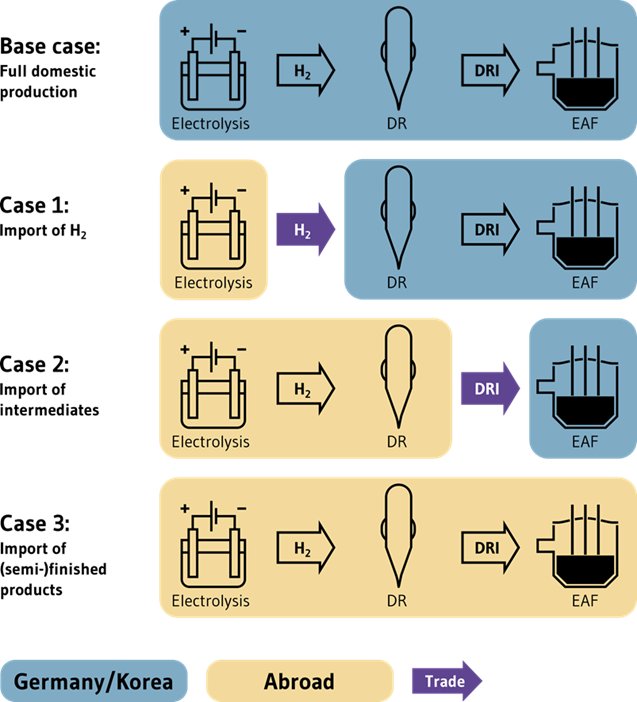

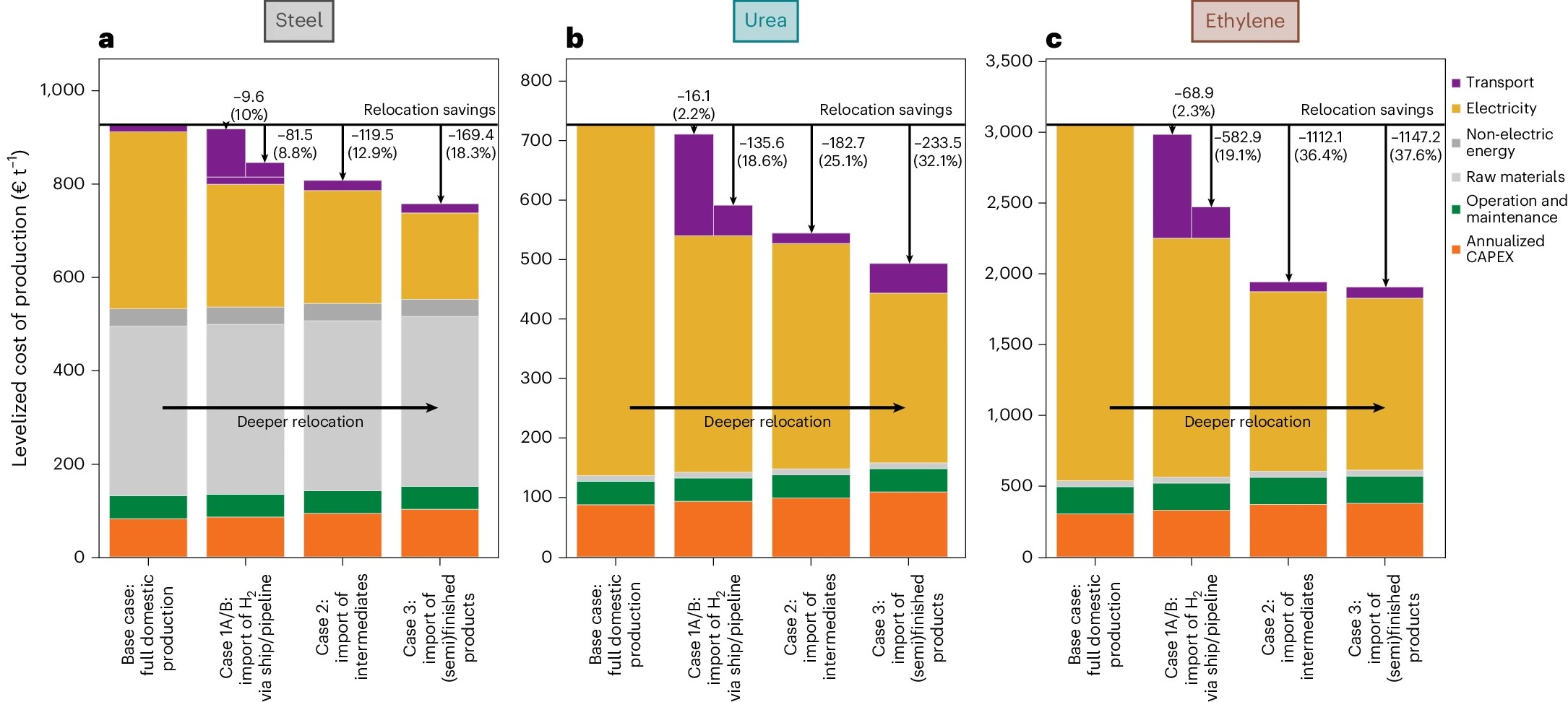

Example 2: Comparing value-chain configurations to quantify the “renewables pull”

Meeting climate targets requires a fundamental transformation of basic materials industries (e.g., steel and chemicals). Low-cost renewable electricity and hydrogen-based processes can make green materials competitive. However, renewable resource quality varies sharply across locations. Regions with abundant, low-cost renewables can therefore gain a structural energy-cost advantage—often described as “renewables pull.” As a result, the energy transition could reshape the global geography of materials production and trade.

Using a relatively simple, generic TEA, we compare production costs for green steel, green ethylene (for plastics), and green ammonia and urea (for fertilisers) across alternative value-chain configurations. We contrast:

- a base case configuration, where production remains in renewable-constrained regions (e.g., Germany, South Korea, Japan), with

- reconfigured supply chains (case 1-3), where energy-intensive steps are relocated to renewable-rich regions (e.g., Northern Sweden, North African countries, the Middle East), and intermediate or final green products are imported for further processing in renewable-constrained regions.

For example, today’s steel production and demand centres could import green iron (hot-briquetted iron, HBI) instead of iron ore, and then convert HBI to steel locally—potentially combining competitive renewable-based primary production with existing downstream industrial clusters and energy infrastructure.

Publication: Verpoort, Ueckerdt et al., Impact of global heterogeneity of renewable energy supply on heavy industrial production and green value chains. Nature Energy 9, 491–503 (2024). https://www.nature.com/articles/s41560-024-01492-z